Corporate Earnings Summary: Walmart (WMT)

Walmart reiterated its full year fiscal 2027 net sales growth targets of 3.5% to 4.5% and adjusted operating income growth of 6.0% to 8.0%.

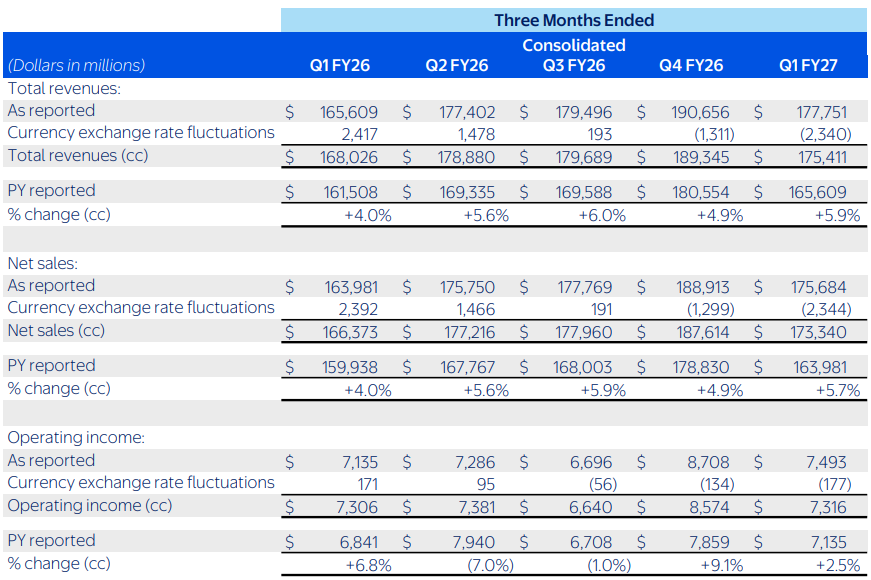

Walmart Inc. reported its first quarter fiscal year 2027 financial results on May 21, 2026, demonstrating continued growth in top line revenue and a significant expansion of its digital footprint. Total revenue reached $177.8 billion, a 7.3% increase year over year, outperforming consensus forecasts by approximately $2.97 billion. This growth was anchored by steady brick and mortar performance and an acceleration in omnichannel adoption, with global e-commerce sales rising 26%.

Operating income expanded by 5.0% to $7.5 billion, or 5.1% on a constant currency basis. Profitability gains from business mix optimization and automation were partially offset by a 250 basis point headwind caused by higher fuel costs across the company’s distribution and fulfillment networks. Generally accepted accounting principles diluted earnings per share came in at $0.67, while adjusted diluted earnings per share stood at $0.66, meeting market expectations.

Despite robust operational metrics and continuous market share gains among value conscious and higher income demographic groups, equity markets reacted negatively following the announcement. This compression reflects investor scrutiny surrounding forward guidance and cost management, as the company reiterated its full year fiscal 2027 net sales growth targets of 3.5% to 4.5% and adjusted operating income growth of 6.0% to 8.0%, maintaining a conservative posture in an unpredictable macroeconomic environment.

Business Description and Strategic Framework

Walmart operates as a global retail powerhouse, utilizing an omni-channel operational template designed to provide consumers with access to a broad assortment of goods and services whenever and wherever they choose to shop. The company has moved beyond its traditional identity as a physical big box merchant, re-engineering its entire corporate structure to integrate digital commerce, logistics infrastructure, advertising networks, and data analytics.

Strategic Priorities

The core corporate strategy is centered around three primary levers aimed at scaling profitability and improving return on investment:

Customer Centric Omnichannel Execution: The seamless blending of physical supercenters with a high velocity digital marketplace. Walmart leverages its physical footprint of over 5,000 domestic units as decentralized fulfillment nodes, enabling rapid store fulfilled pickup and delivery services.

Business Mix Transformation: Shifting the revenue mix toward structurally higher margin digital service streams. This includes the expansion of the global advertising business, marketplace merchant fees, data monetization, and recurring subscription fees from membership initiatives.

Logistics and Automation Scale: Investing heavily in supply chain modernization. The business is deploying automated storage and retrieval systems across its distribution centers and implementing agentic artificial intelligence solutions to optimize inventory routing, reduce final mile fulfillment costs, and expand order density.

Segment Performance

Walmart manages its operations through three main reportable business segments: Walmart U.S., Walmart International, and Sam’s Club. Each unit serves a distinct strategic purpose within the broader corporate ecosystem.

Walmart U.S.

Walmart U.S. remains the foundational engine of the enterprise, accounting for the vast majority of total revenues and operating profits. For the first quarter of fiscal year 2027, the segment recorded comparable store sales growth of 4.1%, excluding fuel. Growth was characterized by positive transaction volume alongside an expanding average ticket size.

The primary catalyst for domestic outperformance was e-commerce, which contributed approximately 530 basis points to the total comparable sales figure. Store fulfilled pickup and delivery services experienced high demand, driven in part by an influx of higher income households seeking convenience. The domestic gross profit rate edged up by 6 basis points, supported by careful inventory control and price optimization, though distribution expenses felt the pressure of elevated fuel costs.

Walmart International

Walmart International comprises retail and wholesale operations across various global markets, including key growth vehicles such as Flipkart in India, Walmex in Mexico, and omnichannel operations in Canada and China. During the first quarter, the international segment delivered net sales growth of 18.0% on a reported basis, or 10.1% when adjusted for constant currency fluctuations.

International e-commerce sales surged 27%, fueled by strong participation in seasonal promotional events and structural improvements in regional delivery logistics. The international segment also benefited from a strong global advertising trajectory, allowing it to build a more resilient margin profile despite the logistical complexities and inflationary pressures native to disparate geographic operating areas.

Sam’s Club

Sam’s Club operates as a membership only warehouse club model, focusing on high volume, limited SKU assortments for individuals and small business owners. The segment delivered net sales growth of 6.1% during the quarter. Comparable sales patterns were solid, supported by positive physical traffic and a 23% increase in segment e-commerce sales.

Membership fee revenue globally grew 17.4%, with Sam’s Club experiencing consecutive periods of high renewal rates and new member acquisitions. The integration of digital tools, such as scan and go checkout technologies and curbside pickup options, has systematically reduced operational friction, helping the club model convert low margin unit sales into highly predictable, high margin subscription income.

High Margin Growth Engines

The foundational retail business is increasingly supplemented by capital light, high margin business lines that alter the financial profile of the enterprise.

Global Advertising

Walmart Connect, the company’s retail media network, grew its global advertising revenues by 37% during the quarter. In the United States, advertising revenue expanded by 36%, benefiting from the integration of the recently acquired VIZIO ecosystem. Retail media allows brands to target consumers directly at the point of purchase using authenticated first party data, converting standard store traffic into high margin ad revenue that flows directly to the operating income line.

Marketplace and Memberships

The third party marketplace continues to expand as fulfillment services are extended to external sellers. This expansion reduces inventory risk for Walmart while generating steady fulfillment and referral fee revenues. Concurrently, subscription revenues via Walmart+ and Sam’s Club memberships grew double digits, providing upfront cash flow and reinforcing customer retention.

Financial Analysis and Tabular Data

Walmart’s consolidated balance sheet and income statement reflect a business in transition, characterized by elevated capital expenditures directed toward supply chain automation and technological development.

Operating cash flow for the first quarter of fiscal year 2027 stood at $4.7 billion, representing a year over year decrease of $0.7 billion. Free cash flow was negative $1.9 billion, declining by $2.4 billion compared to the prior year period. This contraction was driven by the specific timing of inventory receipts, strong unit demand in domestic grocery categories, and higher capital outlays. Global inventory levels grew 8.9% on a reported basis, or 7.8% in constant currency, to $62.6 billion.

The company maintains a strong liquidity position, closing the quarter with $10.7 billion in cash and cash equivalents against total debt of $58.1 billion. During the quarter, Walmart executed $2.1 billion in share repurchases, retiring 16.6 million shares under its new $30 billion buyback authorization established in February 2026.

Consolidated Financial Performance Metrics

Guidance and Outlook

Management has maintained its full year fiscal year 2027 forward guidance, choosing to stay conservative due to shifting consumer behavior and persistent structural headwinds.

For the second quarter of fiscal year 2027, Walmart expects net sales to grow between 4% and 5% in constant currency, with adjusted operating income projected to increase by 7% to 10%. Adjusted diluted earnings per share for the upcoming quarter are modeled in a range of $0.72 to $0.74. For the full fiscal year 2027, net sales growth is expected to land between 3.5% and 4.5%, with adjusted operating income growing 6.0% to 8.0%. Capital expenditures are planned to remain in the range of 3.0% to 3.5% of total net sales, prioritizing automation and fulfillment center conversions.

Analyst Perspectives and Institutional Views

The professional investment community remains divided on Walmart’s immediate upside potential, presenting a contrast between solid structural execution and a demanding equity valuation.

Bull Case: Structural Scale and High Margin Shift

Optimistic analysts emphasize Walmart’s unique position as both a defensive consumer staple play and an expanding digital platform. Institutional researchers point out that the economics of e-commerce are turning a corner. As delivery density increases, local routing and batching efficiencies scale, allowing incremental digital sales to carry higher margin profiles than traditional physical store sales.

Furthermore, analysts view the adoption of contextual, agentic artificial intelligence tools—such as the Sparky shopping assistant—as structural differentiators. These tools have demonstrated an ability to increase basket sizes by roughly 35% among active users, transitioning digital search from a paid traffic acquisition strategy into an organic demand capture mechanism. The high margin contributions of Walmart Connect and international marketplace fees are seen as powerful tools to permanently lift the consolidated operating margin above its historic ceilings.

Bear Case: Valuation Overstretch and Operational Friction

Conversely, cautious market observers point out that the company’s current price to earnings ratio, which hovers above 48x, leaves almost no margin for operational error. The sharp 7% selloff following a solid earnings beat indicates that the market has already priced in an ideal execution scenario.

Skeptics emphasize the persistent risks embedded in the business model, notably the impact of rising fuel costs on distribution expenses, intense competitive pressures from pure play digital operators, and regulatory hurdles such as Maximum Fair Price legislation. There is also concern that while the top line continues to grow through food and grocery categories, higher margin general merchandise categories remain slow to recover, exposing the company to product mix imbalances if inflation continues to strain lower income household budgets.